Months ago, I requested a copy of my Intuit data to see what’s been tracked through my Mint account the last 12 years I’ve had it open. Well they weren’t kidding that it’d take up to 45 days to process the request. I requested it in early Feb and I finally got the download link in mid-March! amazing over a month to make a data dump!

What was inside?

After over a month of waiting, I ripped open the download to find that it’s a bunch of text files saved in JSON format. There wasn’t anything useful inside of the files. The budget data was unlabeled, and transaction data was unlabeled. Here’s an example of it looks like after I formatted the extracts in R so I could actually read them.

I think this is transactions but it’s really light on details, and IDK how I would have so many.

There’s a lot data in the files, but a lot of it is actually 100% unlabeled. I’m not sure what Intuit was thinking, but the data is completely unusable and doesn’t even match the “Export All Transactions” button that’s on Mint.com on the transaction list button.

How to read your Data.

If you’re familiar with R, I basically used the step below to read thru most of the data.

The main file that looked like it had some meat was 10+mb in my extract and located in the Mint sub-folder and had a name like mind_data_78438432894932482339jdjfd.txt. Here’s the code I used to read the data in R:

library(rjson)

#update the working directory and mint_data_

setwd("Your working directory")

con <- file("mint_data_YOUR FILE NAME.txt",open="r")

#read in the file, there might be an error

line <- readLines(con)

#the main file has a bunch of JSON objects, mine had 22, So this step splits them up

split_vars <- strsplit(line, "\\]")

#22 sub objects, I basically just went thru each one by updating X and re-running to see what was in it

x <- 1

mint_data <- as.data.frame(do.call(rbind, fromJSON(paste0(split_vars[[1]][x],"]"))))

For my data extract, these were what I think I saw in the extract:

#1 Personal Info: Most of it was wrong though

#2 Opt ins

#3 User actions?

#4 IDK what this is

#5 Something about banks mostly empty

#6 Something about stocks has my old stocks

#7 Stocks

#8 Budget, but unlabeled

#9 Goals, I don’t use these but the data looked clean

#10 Transaction types

#11 Transactions

#12 Account information

#13 Loans

#14 Something about credit card balances

#15 ?

#16 Currency

#17 Account ids

#18 Currency?

#19 Currency?

#20 Credit cards?

#21 Currency?

#22 Accounts and status

How to get a copy of your Data

If you’re still interested to see if maybe you’ll have better luck than me, here’s how you request a copy of the data they have. You can navigate to this page from Mint by clicking on Settings > Intuit Account > Data & Privacy > Request an extract of your data

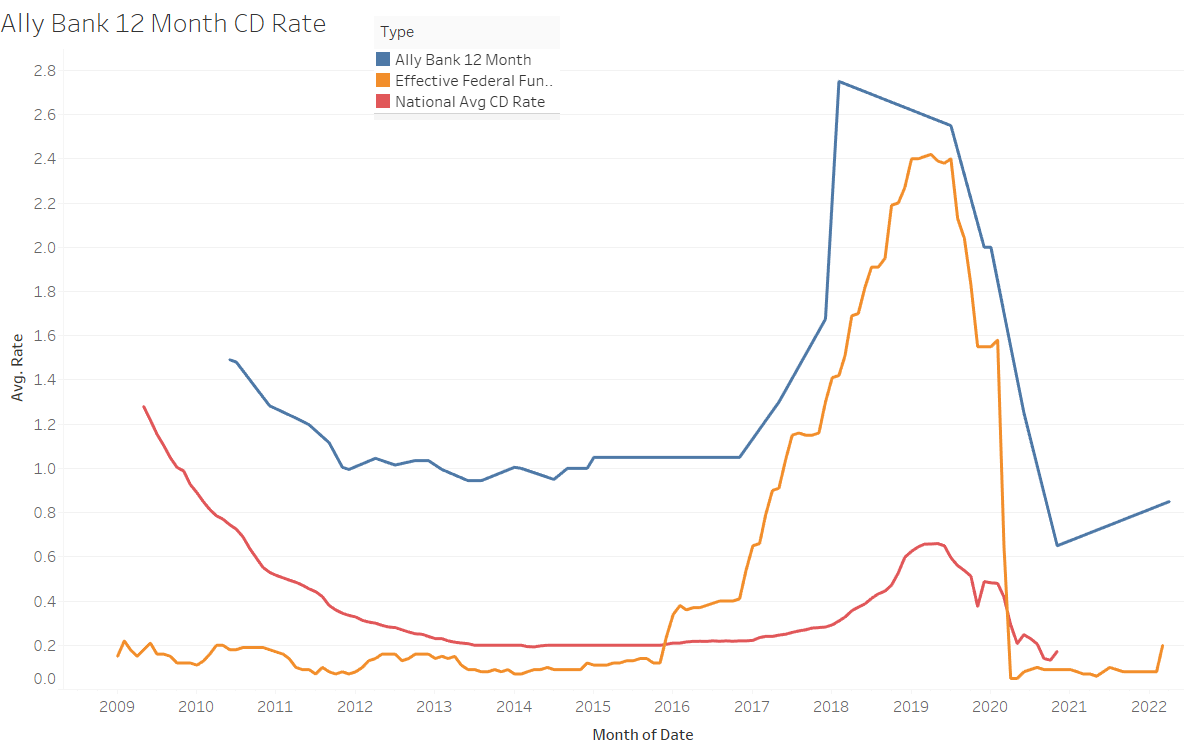

Graph of the Ally Bank CD rates (APY) vs the Federal Funds Rate and National Average CD Rate.

I included the Federal Funds Rate (source: St Louis Fed, Federal Funds Rate) as a comparison as this is the rate that banks lend to each other. You can see the spike in Ally Bank rates generally following increases and decreases with changes to the Federal Funds Rate. So if you’re on the fence about figuring out when is a good time to lock in a rate with Ally Bank on a CD, just look at how the Federal Funds rate has been trending.

In addition, I included the national average for the 12 month CD rates (source: St Louis Fed Avg 12 Month CD). This average seems to be less responsive to the Federal Funds rate, but still shows some similar movement. The 12 month CD rate feed apparently was discontinued, but I’ll leave it up for now since CD rates in the missing time frame (2020-2022) have basically been <1%.

Note for anyone else, I had some trouble with the Web Archive providing inconsistent results on the pages I was using to get the interest rates from. This is why for some of the more recent recordings, I used blog posts to get the rates. I think there is some kind of issue with how the data is saved since it looks like the data is loaded by javascript I think my browser is caching the javascript file with information from a previous snapshot.

Dang the stock market did really well this year. As a result for the first time ever, my net worth increased by more than my total gross income for the year (just barely though). That was a shock.

You don’t have to be particularly skilled at investing when VTI which is Vanguards ETF for the entire stock market, goes up 27.7% (plus 2.12% dividends) with out you doing anything.

Bring on 2020

Have a Happy New Year, and good luck next year! Who knows what it will bring.

I’ve been getting a lot of advertisements touting the salary increases from getting an MBA or a Masters in something else business related. But with any adverisment, is it really worth it?

I decided to look at this from two angles:

You want to stay an individual contributor

You want to move into management

Is it worth it if you don’t want to be a manager?

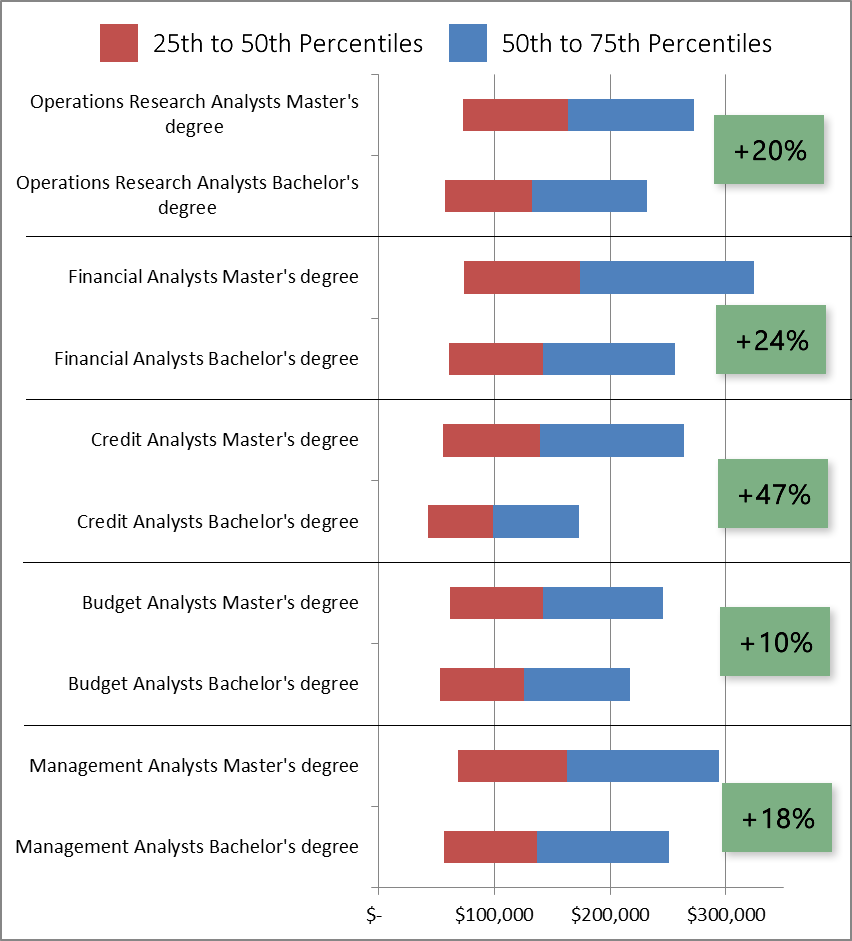

I don’t doubt that a lot of people get a bump from it, but I think that some of the people getting a bump from an MBA are transitioning from being individual contributors like analysts or data scientists to becoming people managers. As a result for people who don’t want to do that, I decided to investigate if it was still worth by using data from the American Communities Survey (2013-2017) and comparing the income distributions for individuals in the same occupation and age group (30-40 years old) by their education either a bachelors degree (any field) or a masters degree (ex MA, MS, MEng, MEd, MSW, MBA).

Results from the analysis

For analysts of different types, you can see that there are median increases to wages ranging from 10% to 47%. Compare this to the nominal value of this translates to between $7k to $26k per year depending on the occupation.

Compare this to the cost of a MBA’s or other related masters programs which comes to $50k to $150k to complete a full course depending on the quality of the program. Since we’re comparing the median graduates before and after, you’ll have to use your own judgement into your calculations. These increases aren’t huge if the program has a list price of $50k, but you’re going to only expect to bump up $15k in the case of an Operations Research analyst. Some quick math says it will take at least 3.3 years to make back that amount without taking into account any tax implications or opportunity cost. In fact, one important thing to note though is that the 75th percentiles for masters degree holders is much further out than for BS degree holders so your ceiling will probably increase as well.

Is it worth it if you want to move into management?

It’s hard to say if people get MBA’s and become managers or if the people who get MBA’s want to be managers and already have the qualities needed to do that but just need some extra qualifications to make it.

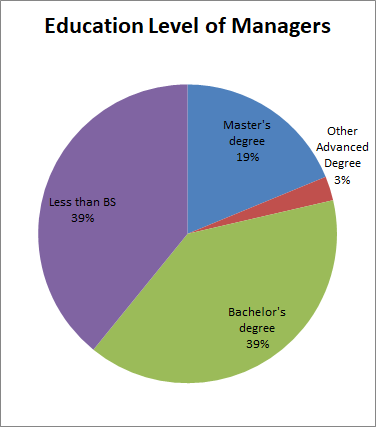

Using the same data table we can see that the portion of managers in these areas who have masters degrees is substantial at 19% compared to 11% for the working population aged 30-40 years old, suggesting that it helps if you get a masters degree but it isn’t a requirement in all management areas.

Masters degree holders are 19% of all Managers, but only 11.3% of workers aged 30-40 years old.

Most noteworthy, 3 fields stood out with very elevated levels of masters and doctoral degree holders in management and those were:

Architectural and Engineering Managers (36% Masters, 5% Other Advanced Degree) : Supervise engineers and architects.

Natural Science Managers (39% Masters, 17% Other Advanced Degree) : Supervise the work of researchers, scientists, chemists, physicists, and biologists.

Social and Community Service Managers (35% Masters, 5% Other Advanced Degree) : Many social workers get more advanced degrees and coursework that overlaps with health.

Therefore if you work in one of those areas, you may find more benefit than the median person.

Data Table

Analyst Occupations by Salary and Education Level

Occupation

Education

25th Percentile

50th Percentile

75th Percentile

Management Analysts

Bachelors

$ 56,880

$ 80,000

$ 113,761

Management Analysts

Masters

$ 68,337

$ 94,699

$ 130,853

Budget Analysts

Bachelors

$ 52,950

$ 72,683

$ 91,534

Budget Analysts

Masters

$ 62,051

$ 80,000

$ 103,541

Credit Analysts

Bachelors

$ 42,292

$ 56,819

$ 74,083

Credit Analysts

Masters

$ 56,006

$ 83,691

$ 123,720

Financial Analysts

Bachelors

$ 61,020

$ 80,823

$ 113,761

Financial Analysts

Masters

$ 73,956

$ 100,000

$ 150,000

Operations Research Analysts

Bachelors

$ 57,193

$ 75,580

$ 99,282

Operations Research Analysts

Masters

$ 72,479

$ 91,006

$ 108,725

Proportion of Workers By Education Level

Occupation

Master’s degree

Other Advanced Degree

Bachelor’s degree

Less than BS

Administrative Services

Managers

13%

2%

34%

51%

Agents and Business Managers

of Artists, Performers, and Athletes

8%

5%

45%

42%

Architectural and Engineering

Managers

36%

5%

48%

11%

Chief executives and

legislators/public administration

22%

5%

46%

26%

Computer and Information

Systems Managers

26%

2%

50%

22%

Constructions Managers

6%

1%

34%

59%

Farmers, Ranchers, and Other

Agricultural Managers

3%

0%

23%

73%

Financial Managers

22%

2%

43%

33%

Food Service and Lodging

Managers

4%

1%

23%

72%

Gaming Managers

9%

0%

24%

66%

General and Operations

Managers

12%

2%

35%

51%

Human Resources Managers

22%

2%

40%

36%

Industrial Production

Managers

13%

1%

37%

50%

Management Analysts

33%

5%

43%

19%

Managers in Marketing,

Advertising, and Public Relations

20%

2%

54%

25%

Managers, nec (including

Postmasters)

20%

3%

39%

37%

Medical and Health Services

Managers

24%

6%

33%

36%

Natural Science Managers

39%

17%

38%

5%

Other Business Operations and

Management Specialists

25%

3%

48%

24%

Property, Real Estate, and

Community Association Managers

9%

2%

33%

56%

Purchasing Managers

24%

4%

43%

30%

Social and Community Service

Managers

35%

5%

41%

20%

Transportation, Storage, and

Distribution Managers

7%

1%

25%

68%

Grand Total

19%

3%

39%

39%

Methodology

I pulled the data from the raw American Communities Survey data for 2013-2017 and restricted to individuals between the ages of 30-40. The average MBA student is 28, so I decided to focus on the age range after where most of the people would have graduated. After extracting the data, I ran some summaries to calculate the income percentiles and educational distributions.

I don’t normally go into politics, but this topic seems to touch a little more closely to FIRE, since there are specific growth rate assumptions that were made.

Buried under the headlines over how much Jeff Bezos would be taxed under Elizabeth Warrens Medicare for All plan was a side note on an additional tax to target the top 1% of households by net worth for a new tax called “mark to market.” This tax basically would restructure capital gains to take place every year regardless if there was a sale. Warren’s plans referenced a study freely available, if you’d like to read it yourself. The researchers used the Survey of Consumer Finances by the Federal Reserve, which is what powers many of the comparison calculators on this website.

To be in the top 1% by using total net worth, you would have to have $10.350 million in net worth to be in the top 1% of households based on the last survey results available using 2016 data. The authors don’t mention if they adjusted out any assets from their projections, so I’m going to assume not. The paper referenced by Elizabeth Warren referenced uses a rather optimistic 8.33% return on investments (page 30 of the PDF).

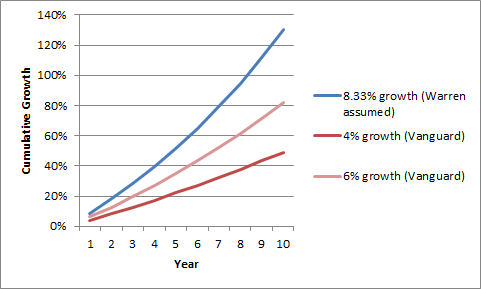

Over estimated returns

Assumptions of the 8.33% used by the paper Warren references (page 30)

Vanguard is projecting a average annual returns of only 4-6% for US equities. 86% of the top 1% are over the age of 50 so their asset allocations are most likely more conservative than the overall stock market, and would likely grow much slower than the 8.33%. So with those 2 factors combined, most likely the $2T incremental tax contribution is very over stated especially considering the effects of lower compounding growth.

Shortfalls will need to be filled with other taxes

Using the 8.33% growth over a decade you would end up with 130% cumulative growth, but with 4-6% over the decade the growth would only be 49%-82% so the taxable gains would be 37% to 69% of the budgeted $2T which would cause a short fall in taxes of $0.6T to $1.3T.

4% to 6% cumulative growth estimated by Vanguard is much lower than the paper that Warren based her budget on, and would provide far lower tax revenues

Months ago, Warren and others had mentioned only targeting the wealthiest of the wealthy for the incremental taxes to pay for Medicare for All among other plans. The first primaries are still months away and Warren’s tax plans have started to dig further and further down the wealth ranks. Sure, people with $10m+ dollars in net worth are probably going to be fine. But if there are shortfall like the one I mentioned, where is the incremental money going to come from? A tax on $1m+ net worth households (top 10% by net worth) doesn’t look as implausible any more as the standards of who should be taxed keeps falling and falling.