Most large companies use a concept called the cost of capital as a factor judge whether or not an investment is worthy to go ahead. This cost of capital refers to the cost of taking on debt to pay for the investment or to the loss of what that money could have done elsewhere.

How does a personal cost of capital translate to my own personal finances?

Using a cost of capital in your personal life can help you to prioritize between paying off loans or investing in yourself, your business, or investments. First, the main concept is that your personal cost of capital should be low risk. Next, your personal cost of capital should have the largest expected payback of your low risk options. It will serve as the bar that any other financial decision needs to meet in order for you to go ahead.

For most people your personal cost of capital will first be:

- The interest rates on any debt that you hold (car loans, credit cards, student loans, mortgages, etc).

- If you don’t have debt, it would be the interest rate on any CD’s or savings accounts.

Everyone’s cost of capital will be different due to varying options and opportunities. It will also change over time as you progress through life.

Example with Student Loans

Let’s say you went to college and have student loans. You’re getting a $1,000 bonus at work. Further, you already have 6 months of savings in your emergency fund. You aren’t sure which of these options you should take:

- Option 1: Leaving it in your bank account for 1% annual interest.

- Option 2: Paying an extra $1,000 to your $10,000 student loans. These loans are at 6.8% annual interest and have 10 years remaining.

- Option 3: Paying to take a certification which will earn you a $100 raise at work every year for the next 10 years. This equates to a non-compounding 10% interest rate.

Basic Analysis

- Option 1 will net you $105 over 10 years and is very safe, using the interest formula, [Ending amount] = [Starting Amount] eAnnual Interest Rate * Number of Years

- Option 2 will net you a guaranteed $875 over 10 years. This was calculated by summing up $3,809 in interest without the extra payment, versus $2,934 with the extra payment. I used this student loan payback calculator from Bankrate.

- Option 3 may net you $1,000 over 10 years. But, there is some risk, because maybe you will move to another employer in those 10 years.

In a business, we would look at these options and say, Option 2 is the cost of capital that we’re going to use to compare the other options against. It has a good return, low risk, and low effort. Your next decision would be whether or not to go for option 3. It has an even higher payback, but would require more research on what your plans and goals are in the future.

This concept should help structure your thoughts around how financial decision is going to affect you. Finally, there are going to be a lot of other factors that will impact your final decision. Your personal cost of capital is a small piece to help to put numbers around it. But, remember money is a tool not the goal, so put your money to the best use.

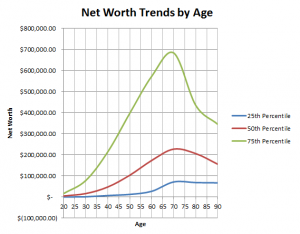

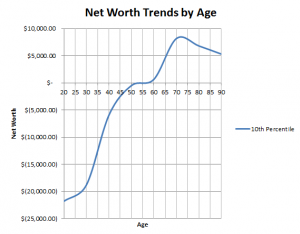

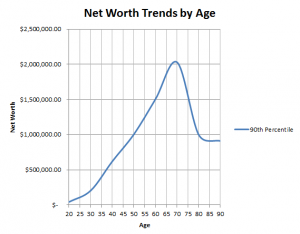

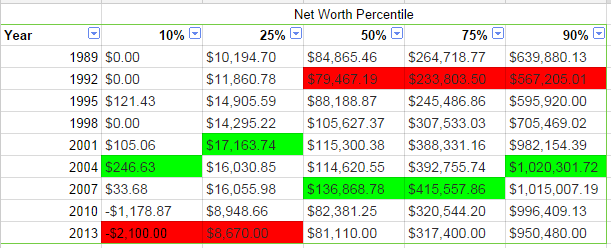

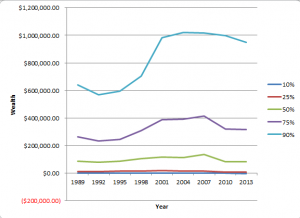

For further reference here are those same numbers plotted to show the relative changes in wealth between Americans at the 10th, 25th, 50th, 75, and 90th percentiles. The largest gains in the last couple decades have captured at the 10% and presumably above. I am hesitant to calculate and publish the numbers of the 5th and 95th percentiles because the data is a lot more prone to being skewed at the long tail ends of the distributions.

For further reference here are those same numbers plotted to show the relative changes in wealth between Americans at the 10th, 25th, 50th, 75, and 90th percentiles. The largest gains in the last couple decades have captured at the 10% and presumably above. I am hesitant to calculate and publish the numbers of the 5th and 95th percentiles because the data is a lot more prone to being skewed at the long tail ends of the distributions.{kind=link}